|

We're talking about vehicle damage claims here, NOT auto accidents that involve serious injuries.

Think of it as a HOW TO on navigating the aftermath of an auto collision and what info is important to collect.

The more you know the more likely it'll go smoothly.

"I'm sorry I hit you. I've had a long day of filming Old Navy commercials."

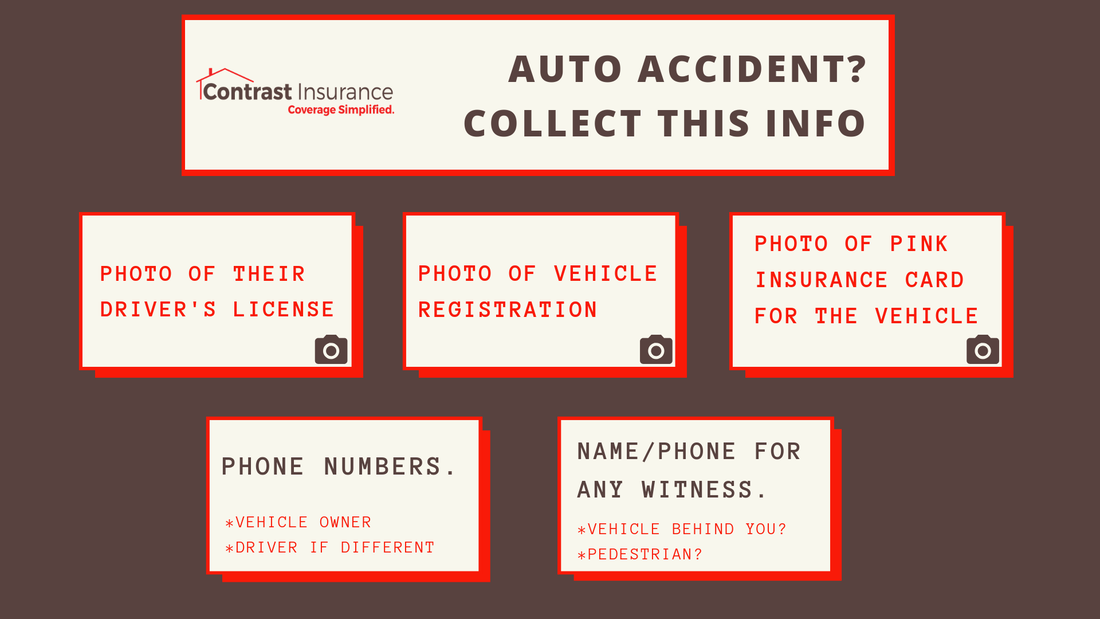

1. IF POSSIBLE....PULL OVER.

If nobody is hurt, move your cars out of the road. Use your smart phone to take a couple photos of the position of the vehicles and pull them out of the middle of the road. It's super dangerous to make others avoid you, and that'll be the first thing the police suggest.

2. KEEP IT TOGETHER.

Even if you're FURIOUS at the other driver...escalating things with someone you don't know is a terrible idea. There is no circumstance where this will help you, and MANY circumstances where it makes things MUCH worse.

Both of you are inconvenienced and you're now in it together...so don't play the blame game. Just get what the info you need and get out of there. 3. USE YOUR PHONE.

Snap a few photos instead of handwriting everything on an old Wendy's bag from your car floor. You'd be surprised how often people write down the wrong policy number/details when they're in this situation. Preserve the data with actual photos of the originals...PLUS it's much quicker.

The below will give you everything you need:

4. CAN YOU GET A WITNESS?

90% of the time this 'witness' will not be required...but in that 10% of the time when you need them, WOW can they be a difference maker.

A couple points on how Physical Damage claims work:

1. Adjusters determine who is 'at fault' in an accident, usually by taking 'statements' from each driver. (Basically asking them both what happened.)

2. If both drivers have 'conflicting statements' this can lead to a dispute about who is really at fault.

3. Passengers inside vehicles involved DO NOT COUNT AS WITNESSES, so having a stranger who saw it all happen can be a tie-breaker.

Often the 'at fault' party feels bad and willingly provides the factual details of what happened....but NOT ALWAYS.

Allow me to paint a picture.

Driver 1 is sitting in his car inside a parking stall at the local grocery store sending text messages because people do that.

Driver 2 is navigating the parking lot in search of a parking spot so they can go inside and buy a truckload of Chicago Mix Popcorn because it's delicious. Driver 1 is done sending their texts and is ready to finally leave. They cut the wheel and back out of their spot and bump right into the front of Driver 2's vehicle. Damage Overview: Driver 1's back bumper and Driver 2's front bumper. Driver 2's LOSES THEIR MIND on Driver 1 because they've not read this blog post about 'KEEPING IT TOGETHER' and the inevitable delay on the Chicago Mix is setting in. Driver 1 has gone from feeling bad, to wanting to do it again. After they exchange information and leave, they decide their recollection of the events was that they pulled out, and started driving away when Driver 2 RAN INTO HIM.

The damages support both versions of events and without an independent witness, or video proof....it could end up with both drivers being held 50% at fault.

Fictional story, but totally possible.

MORAL OF THE STORY?

FIND A WITNESS IF YOU'RE IN AN ACCIDENT. OFFER TO BE A WITNESS IF YOU SEE AN ACCIDENT.

What if Driver 2 were alert enough to find someone else who saw it all happen?

Grab their info, and go get that Chicago Mix so the trip wasn't a total waste. MD

2 Comments

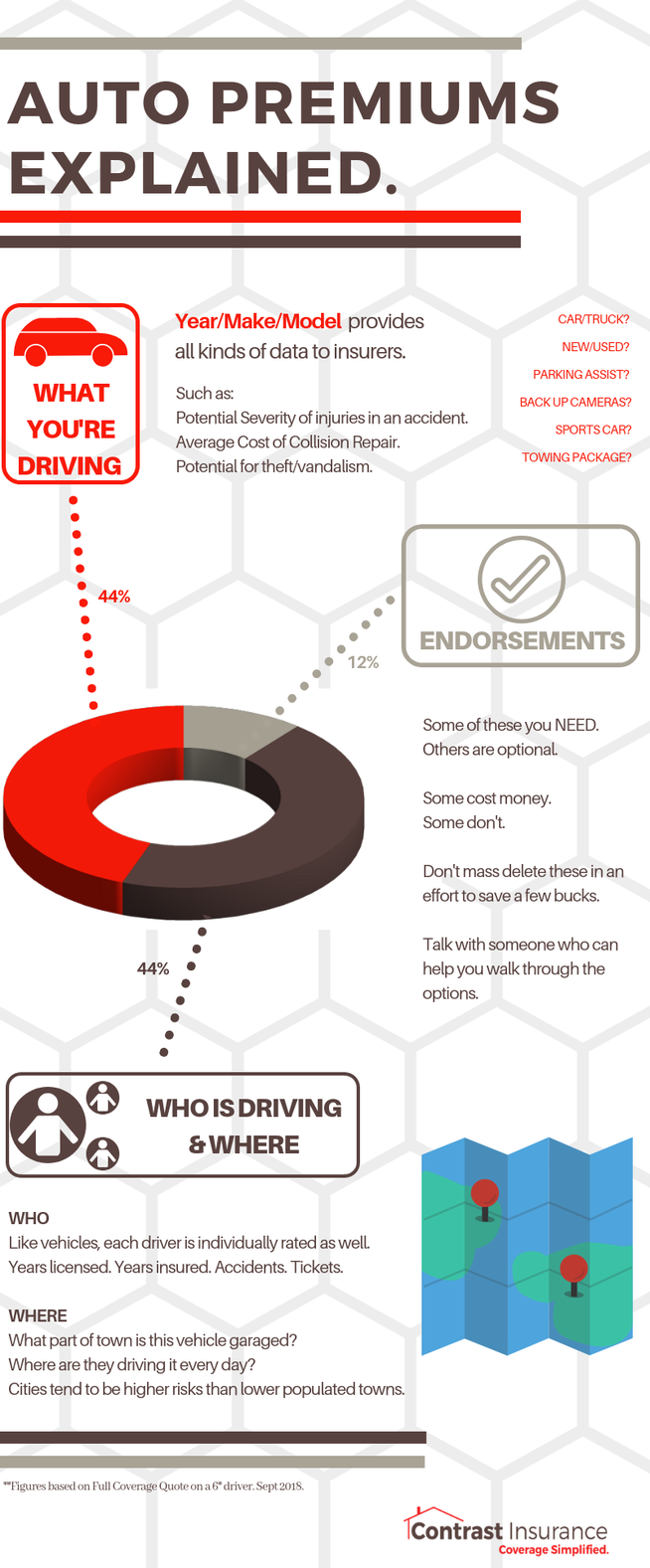

What's a good deductible for my insurance?If you've ever had insurance before, chances are you've heard the term 'deductible'. Let's just go ahead and define it: It's the amount of money a policyholder is responsible for in the event they make a claim on their policy. WHY IS THIS IMPORTANT? Well one reason is that DEDUCTIBLES are typically DIRECTLY RELATED TO THE COST OF THE INSURANCE POLICY. The MORE money a person is willing to pay for a deductible, the LESS money an insurer usually charges for the policy. Another IMPORTANT reason to care about your deductible is that you should MAKE SURE YOU CAN AFFORD TO PAY IT IF YOU NEED IT. *So don't get carried away with $5,000 deductibles on your 2006 Honda Civic. 2 Deductibles - 1 PolicyThere's nothing new about the idea of multiple deductibles in one policy. Consider Auto Insurance being split into collision and comprehensive deductibles. What's WORTH KNOWING NOW - Is how this has made it's way into both HOME INSURANCE and COMMERCIAL PROPERTY INSURANCE. Many insurers will give you a $500 or $1,000 deductible on the house....but then require a $2,000 deductible for any WATER damages. In some cases they may remove or limit coverage on certain types of damage altogether. Ex. Vandalism by tenants. The reasoningBy PUSHING UP DEDUCTIBLES insurers hope to: 1) decrease the number of small claims being made. 2) ease the pressure of yearly premium increases. 3) make policyholders care more about AVOIDING losses altogether. AdviceDon't apply a one size fits all approach here. Some carriers offer GREAT price breaks for certain deductibles, and way less of a break on the next level up. EXAMPLE: Home Policy costs $1000 a year with a $500 deductible. That carrier may offer you $850 a year for a $1000 deductible. (that's a solid price break if you're wondering) Then $800 a year for a $2,500 deductible. The last option is not as attractive in my opinion, but someone trying to minimize their yearly premium may feel differently. What is reasonable for one family to payout in the event of a loss may not be for another. KEY TAKEAWAYS: 1) Understand what a policy requires of you if you need to make a claim. 2) Be comfortable paying the amount of a deductible if you need to. 3) Minimize the cost of coverage by figuring out what risk you're willing to carry. CLAIM SCENARIO - Deductibles in actionFUN FACT: Did you know a deductible applies to the LOSS and not to a policy limit? Example: Jewelry has a $5000 maximum payout on a policy and a $1000 policy deductible. Policyholder 1 loses their $6,000 engagement ring while taking a ride on the Halifax Harbour Hopper. Lucikly they listened to a broker who helped them purchase a policy that included 'mysterious disappearance'. Most consumers would probably do the math like this: $6,000 ring Maximum jewelry limit is $5,000. LESS the $1,000 deductible = $4,000. .....but that'd be incorrect. The ACTUAL calculation takes a DEDUCTIBLE from the LOSS and THEN applies any policy limits.

$6,000 ring - Deductible (1000) = $5,000 In this case, policyholder 1 would get a $5,000 payout. |

Categories

All

Archives

January 2024

|

RSS Feed

RSS Feed